BY P. GUNASEGARAM | Kinibiz

DECEMBER 14, 2015 8:00AM

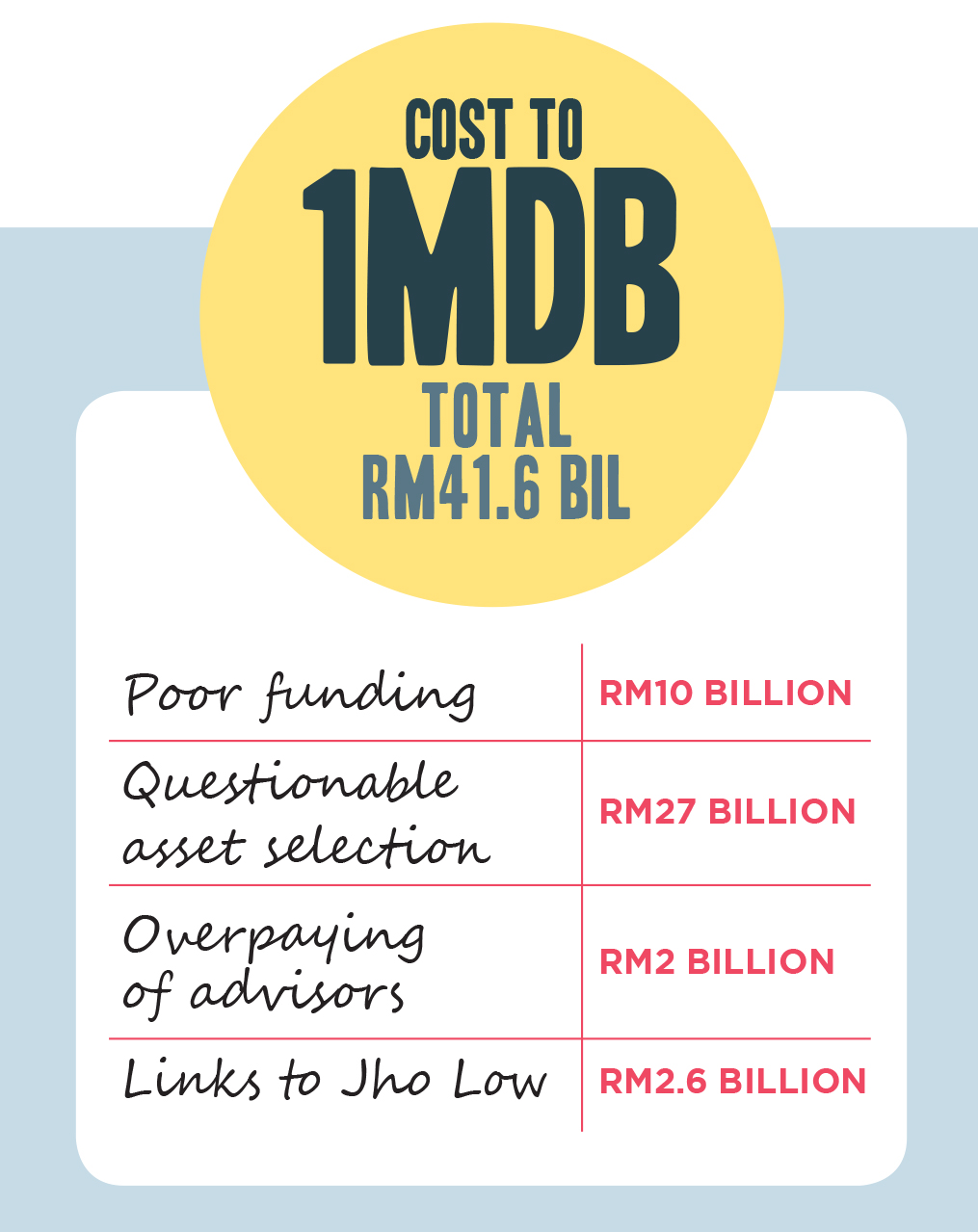

The very setting up of 1MDB and its operations was aimed at spinning billions out of this self-styled strategic development company owned by the government for the benefit of various others. The eventual cost of this to the country might be as high as RM42 billion.

___

[Note to readers: This article and the associated charts provide an overview map of our coverage of 1MDB, and attempt to link the various parts to the whole. The information for the series is obtained from various sources both public and private and includes reported content elsewhere and others from our own sources, which we believe to be accurate. Figures have been rounded off where it makes things clearer.]

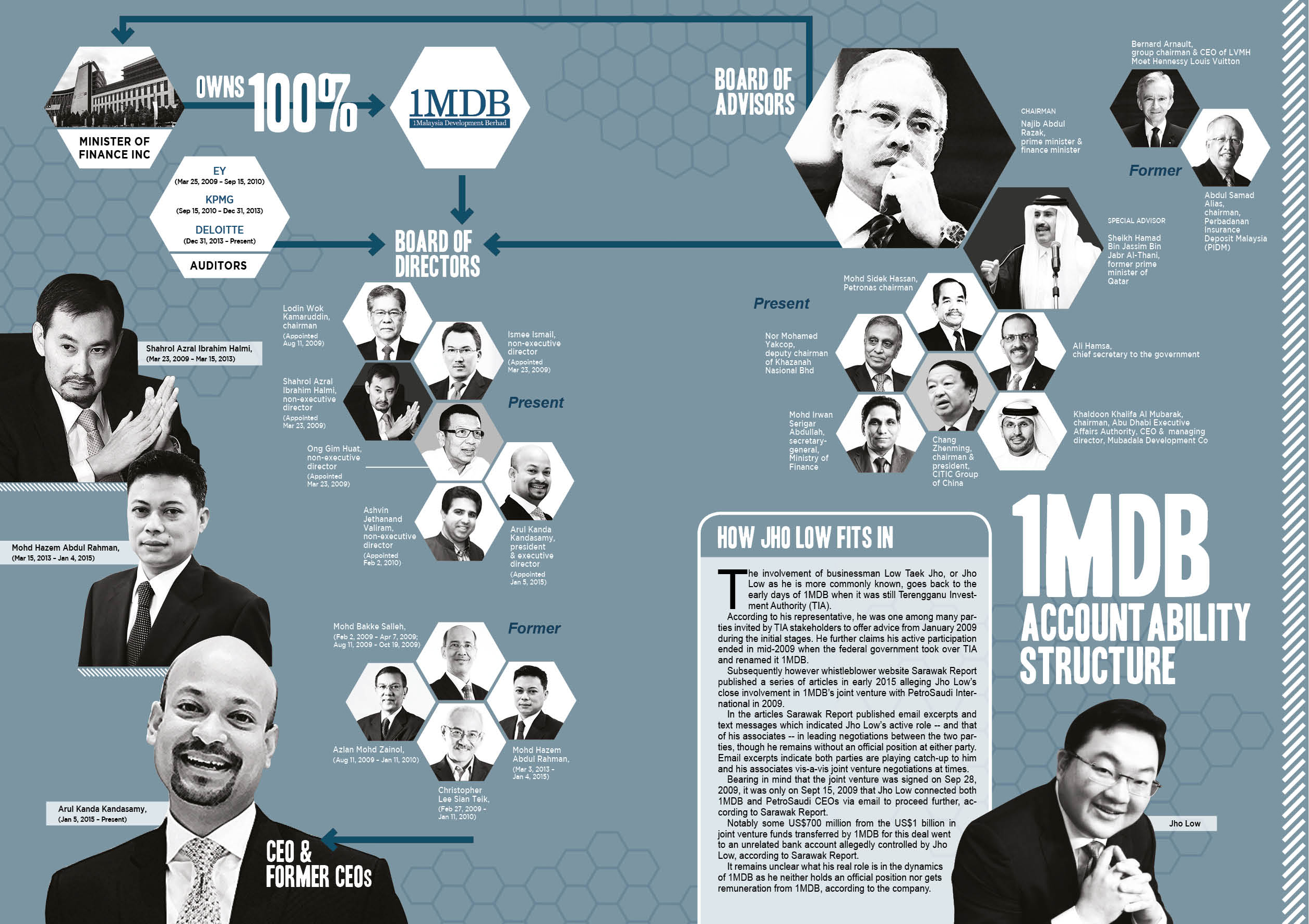

Even before it became 1Malaysia Development Bhd (1MDB), it was mired in controversy as Terengganu Investment Authority (TIA) in 2009, Terengganu’s very own sovereign wealth fund. TIA was to be kickstarted with a RM5 billion bond issue guaranteed by the federal government.

In the same year itself, TIA, whose bond repayment was supposed to have been made from oil royalties to the state, was taken over by the Minister of Finance Inc after both the Sultan of Terengganu and the Menteri Besar objected to financing methods. More on that later.

The brains behind TIA was none other than Low Taek Jho, also known as Jho Low, a well-connected young businessman-whizzkid known for his lavish parties all over the world with well-known celebrities and now reportedly in hiding in Taiwan.

Low and the others associated with the saga that 1MDB has become are dealt with in greater detail in the next article.

He has denied any links with 1MDB, indicating that he merely gave advice when asked and never had any management role. That may be technically correct but a series of email leaks from 1MDB management indicated that Jho Low was intimately involved in the decision-making at an unofficial level.

This eventually culminated in email revelations that US$700 million was transferred in 2009 into the accounts of a company, Good Star Ltd, allegedly related to Low. Good Star was not linked in any way then to any of 1MDB’s transaction.

But even this is just the tip of the iceberg as far as potential losses for 1MDB and the nation – which indirectly owns 1MDB through the Minister of Finance Inc – are concerned. KINIBIZ analysis indicates that the money wasted through various means could be as high as RM42 billion, assuming that there is no recovery from investments into dubious way. And this does NOT take everything into account.

Unsuitable business model

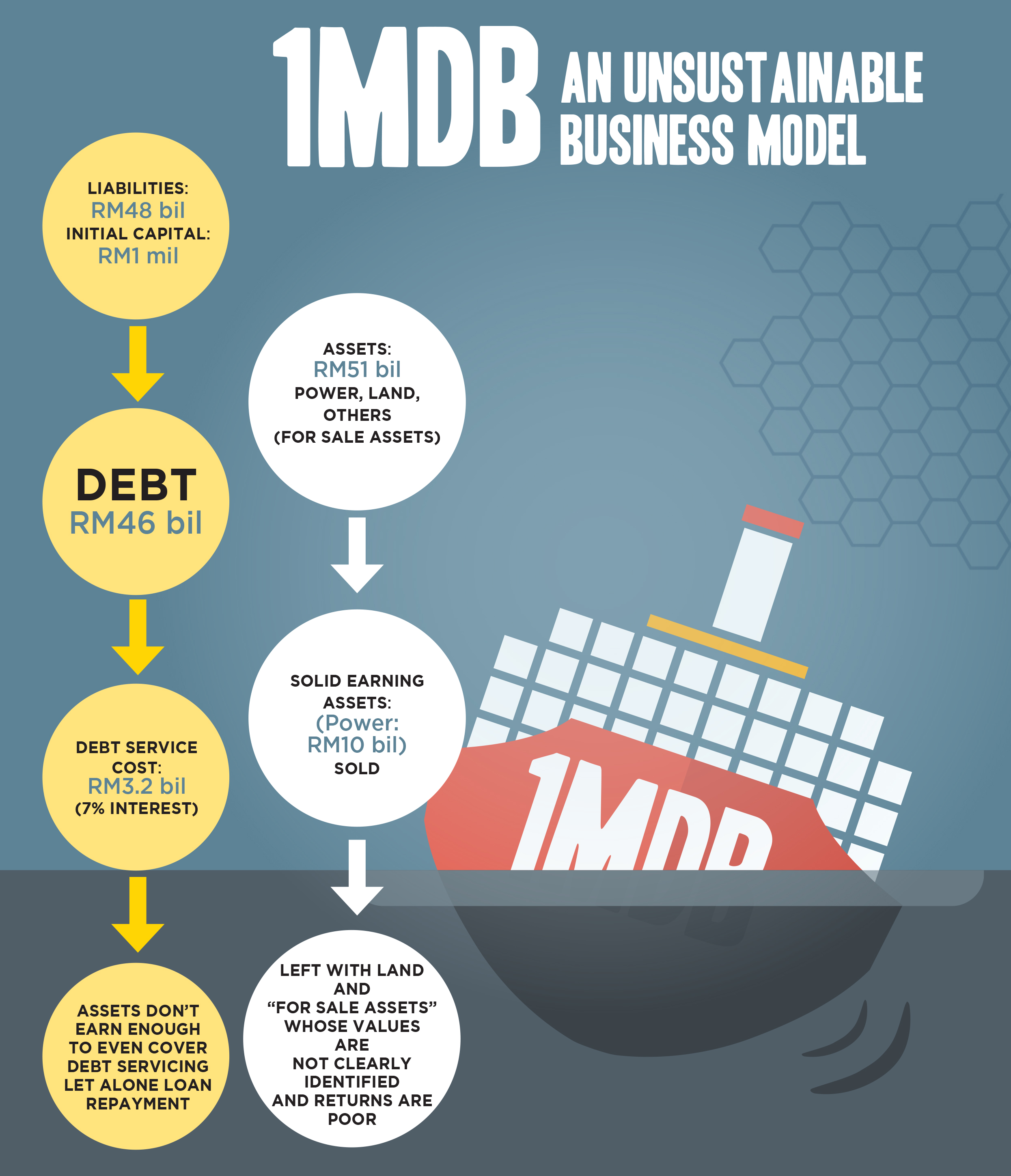

1MDB’s business model from the start was flawed and its reporting line drew alarm bells from way back in 2009 when it was excluded from all the corporate governance measures introduced under the government-linked transformation programme from the mid-2000s. It became a law unto itself and its CEOs often acted in direct contravention to orders from the board.

It was built on an edifice of debt – RM1 million in initial capital as against RM46 billion in debt – that’s a gearing ratio of 46,000 times! The subsequent equity level of RM2.44 billion was due entirely to revaluation of properties injected cheaply into 1MDB.

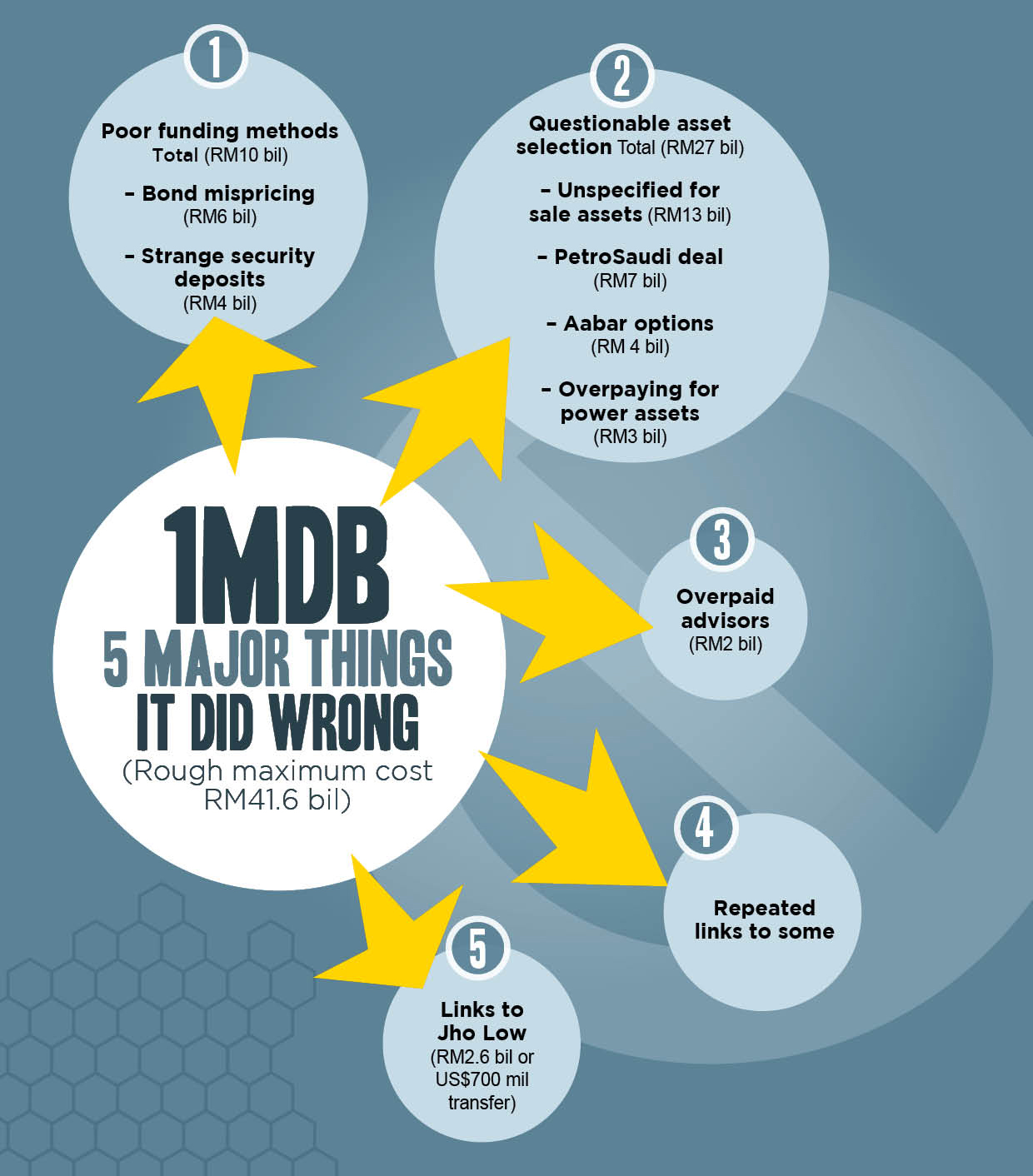

1MDB, its management and co-conspirators outside the company used five main ways to siphon billions out of the company. They were:

Poor funding methods (RM10 billion)

This started with the RM5 billion bond issue arranged by AmBank group where the bonds were mispriced by giving higher coupon rates to selected investors. This was repeated in subsequent US dollar bonds arranged by Goldman Sachs. Such mispricing could have accounted for as much as RM6 billion.

This started with the RM5 billion bond issue arranged by AmBank group where the bonds were mispriced by giving higher coupon rates to selected investors. This was repeated in subsequent US dollar bonds arranged by Goldman Sachs. Such mispricing could have accounted for as much as RM6 billion.

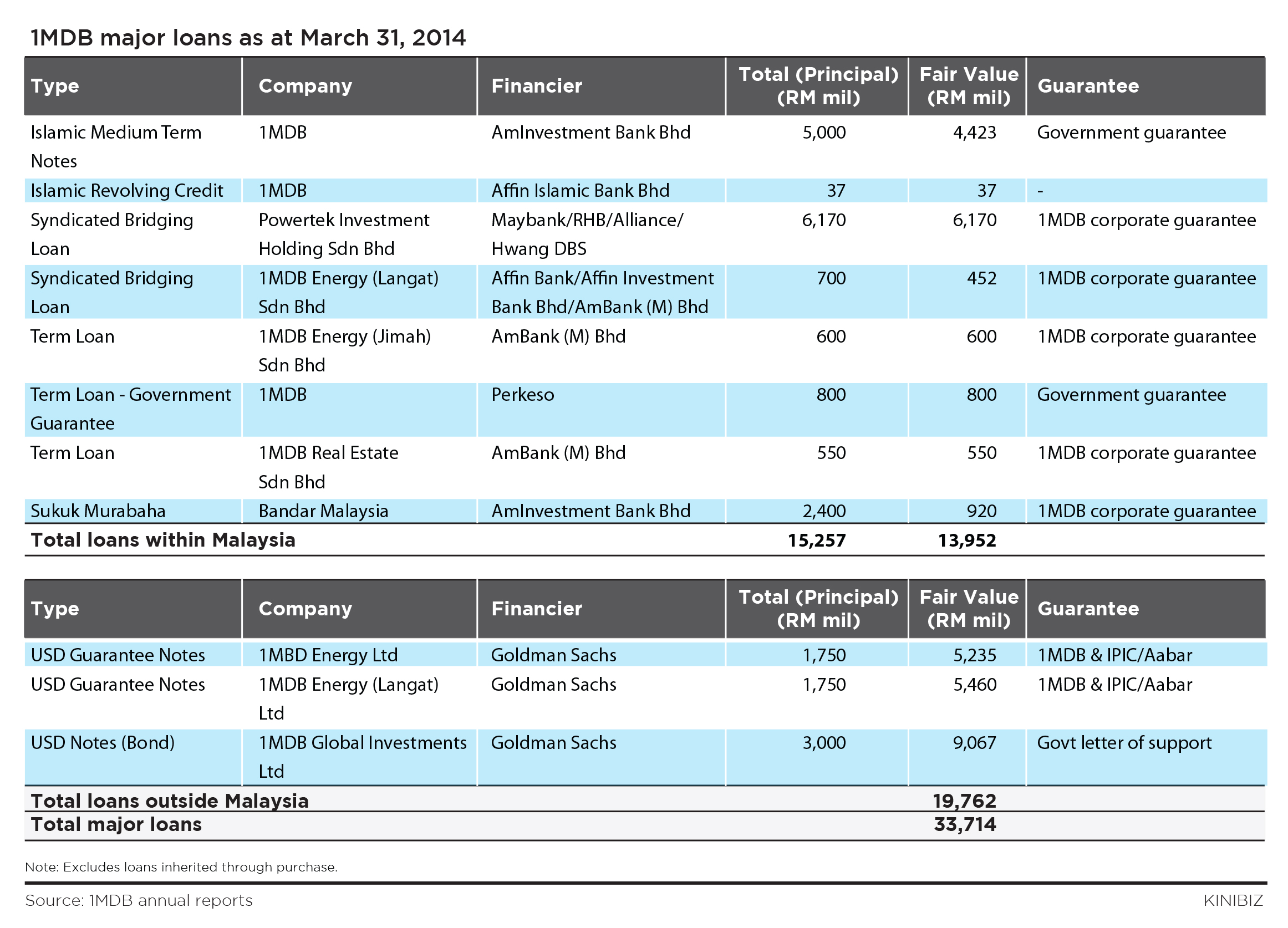

On top of that, there were strange arrangements for some of these loans. For some US$3 billion of loans which were guaranteed by Abu Dhabi’s International Petroleum Investment Co (IPIC), nearly half of the money or over RM4 billion was put back as security deposits with Aabar PJS Investments, a company related to Aabar. 1MDB did not have use for over 40% of the funds it raised while much of the remainder went into a joint venture with IPIC.

Questionable asset selection (RM27 billion)

In its latest available accounts for the year ended Mar 31, 2014, 1MDB had listed some RM13 billion as unspecified assets for sale, which auditors were not able to verify because there was no market for them. It is unacceptable that the fund took tens of billions in loans but yet had intentions to sell those assets.

In its latest available accounts for the year ended Mar 31, 2014, 1MDB had listed some RM13 billion as unspecified assets for sale, which auditors were not able to verify because there was no market for them. It is unacceptable that the fund took tens of billions in loans but yet had intentions to sell those assets.

Other examples include the PetroSaudi deal where all the initial borrowings by 1MDB and more went into PetroSaudi and which to date has not been satisfactorily accounted for. It is through this deal that some US$700 million (RM2.6 billion) was transferred into the account of a company related to Jho Low, a company totally unrelated to the transaction. 1MDB directors had vehemently questioned the transfer and demanded its return but to no avail.

Another example was the payment of some RM4 billion (nearly US$1 billion) to extinguish an option given to Aabar to purchase a 49% stake in the energy assets of 1MDB upon its listing. That’s a crazy price because the entire power assets when purchased were around RM12 billion to RM13 billion; 49% would be worth no more than RM6.5 billion. The RM4 billion price for an option is therefore worth over 60% of the underlying asset!

Another example was the payment of some RM4 billion (nearly US$1 billion) to extinguish an option given to Aabar to purchase a 49% stake in the energy assets of 1MDB upon its listing. That’s a crazy price because the entire power assets when purchased were around RM12 billion to RM13 billion; 49% would be worth no more than RM6.5 billion. The RM4 billion price for an option is therefore worth over 60% of the underlying asset!

Finally, there was the overpayment for power assets by an estimated RM3 billion.

The question is why did 1MDB undertake these transactions which could incur losses of as much as RM27 billion in total? Basically, to benefit others, not 1MDB.

Overpaying of advisors (RM2 billion)

One firm, Goldman Sachs, could have got billions of ringgit in fees. Such overpayment could have accounted for as much as RM2 billion. Fees for just US$1.75 billion in bonds, accounted for some US$200 million in one instance, or an unheard of 11.4% of such a huge issue.

Repeated links to the same people

These include some unsavoury people in some major projects, eg PetroSaudi. Others are Abu Dhabi, joint-venture partners in Bandar Tun Razak and convoluted deals involving IPIC and Aabar. And finally, the Qataris in the Bandar Malaysia project. Why is there a need to get foreign investors into land projects where we have plenty of expertise within Malaysia?

Links to Jho Low (US$700 million, RM2.6 billion)

Despite his denials and the denials of 1MDB, Jho Low played a massive although background role in 1MDB, influencing management behind the scenes and eventually there was a transfer of US$700 million to a company related to him out of a 1MDB unit.

Despite his denials and the denials of 1MDB, Jho Low played a massive although background role in 1MDB, influencing management behind the scenes and eventually there was a transfer of US$700 million to a company related to him out of a 1MDB unit.

Basically, all these show that 1MDB is indeed in dire straits. Its loan and interest obligations of over RM8 billion post-2014 could not be met from cash flow and hence the need to continue to borrow and to roll to hide its true situation where its viability as a going concern is already under serious threat.

Current management assertions that obligations will be met is only because further loans have been taken and disbursed and the sale of better quality assets, for example power for RM10 billion, and property represent desperate attempts to inject liquidity to stop it from going under.

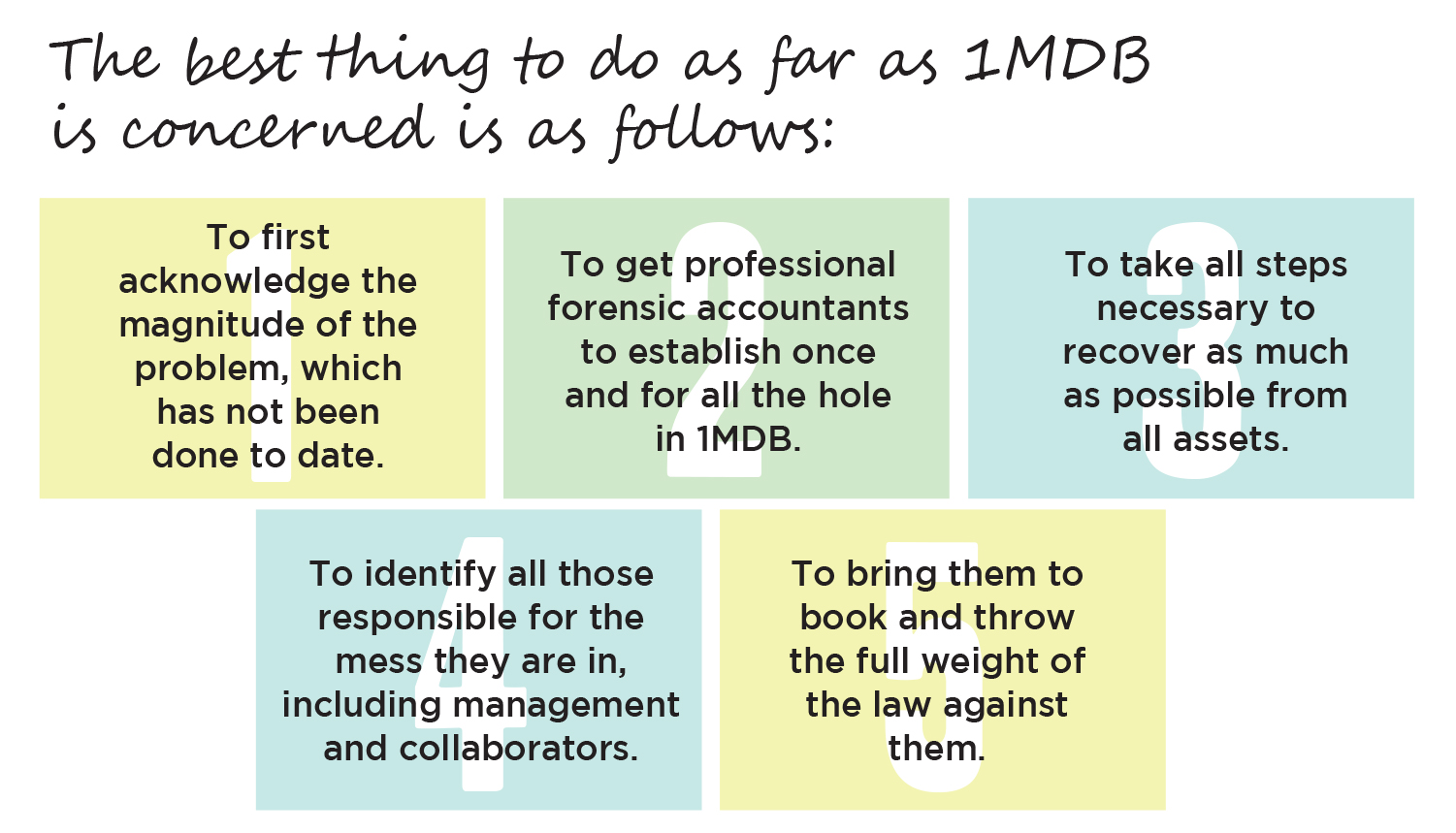

The best thing to do as far as 1MDB is concerned is as follows:

- To first acknowledge the magnitude of the problem, which has not been done to date.

- To get professional forensic accountants to establish once and for all the hole in 1MDB.

- To take all steps necessary to recover as much as possible from all assets.

- To identify all those responsible for the mess they are in, including management and collaborators.

- To bring them to book and throw the full weight of the law against them.

But that’s not likely to be done any time soon.

[click to enlarge]

[click to enlarge]

Tomorrow : The colourful family and friends of 1MDB

Seeing those bustard to jail will be the best wishes of the year!